The Hidden Value of B2C: Lessons from Historical VC Exits

In the VC space, we often see less excitement around B2C startups, and for valid reasons: higher customer acquisition costs, greater difficulty in retention, and more volatile demand compared to B2B businesses. But if these factors increase risk, the real question is whether B2C companies have historically generated returns large enough to justify taking that risk. My colleague Afaf shared her perspective on this topic in a previous blog; here, I offer my own point of view.

Venture capital is one of the riskiest asset classes. High returns, by definition, come with high risk, and the industry operates under a power-law dynamic, where a small number of portfolio companies generate the majority of returns and compensate for losses elsewhere. While I agree with the B2C risks outlined in Afaf’s blog, examining historical outcomes through the lens of exits, both in terms of volume and value, offers a more nuanced view.

According to historical data published by Sapphire Ventures:

Venture-backed enterprise (B2B) technology companies have generated approximately $1,609B in exit value since 1995 ($622B from M&A and $987B from IPOs), across roughly 7,600 exited companies.

Venture-backed consumer (B2C) technology companies have generated approximately $1,436B in exit value since 1995 ($240B from M&A and $1,196B from IPOs), across roughly 4,200 exited companies.

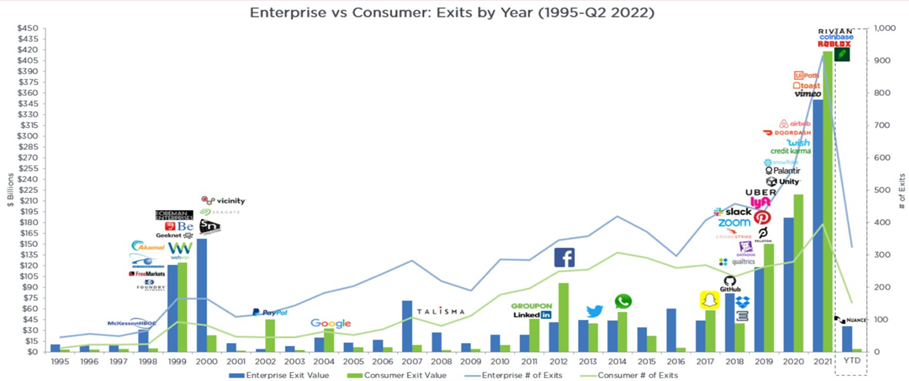

At first glance, these figures appear to favor B2B: total exit value is higher, and the number of exits has consistently exceeded those of B2C across most years. However, a deeper look at how value is distributed tells a different story.

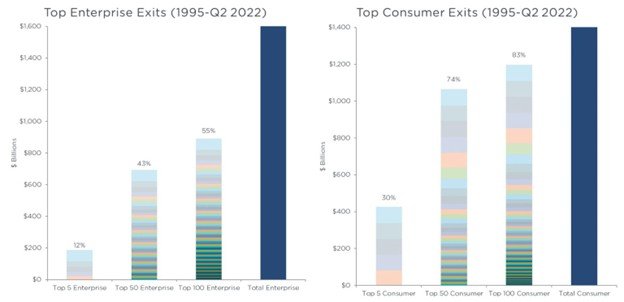

When total exit value is broken down, as shown in the graph below, B2C startups demonstrate significantly stronger outlier performance. The top five enterprise exits account for $188B of the total $1,609B generated by B2B startups. In contrast, the top five consumer exits account for $426B of the $1,436B generated in the B2C category. In other words, the value generated by the top five consumer companies is approximately 2.3x greater than that of their enterprise counterparts.

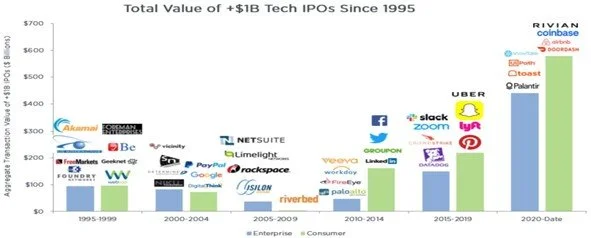

This pattern becomes even more pronounced when looking at large consumer outliers since 2011. Companies such as Facebook, Uber, Snap, and Rivian exited at valuations far exceeding those of the largest enterprise technology exits during the same period. In fact, the top 1% of consumer exits since 1995 have been 140% larger than the top 1% of enterprise exits.

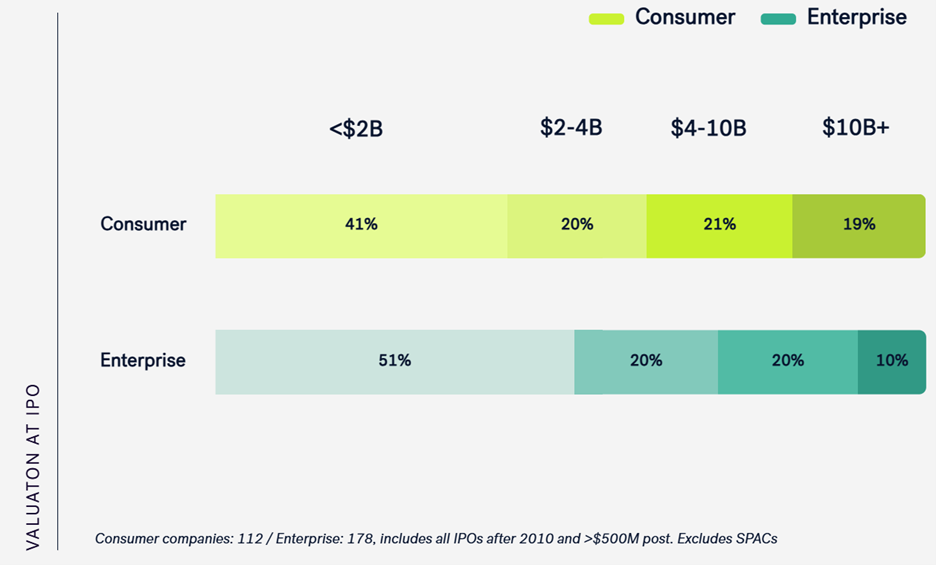

Additional data from Forerunner Ventures reinforces this dynamic: 19% of consumer IPOs achieved valuations above $10B, compared to only 10% of enterprise IPOs.

In conclusion, the data make one point undeniable: B2C companies have the potential to deliver extraordinary value. In a venture world defined by power laws, ignoring B2C opportunities simply because of inherent risks, like high CAC or retention challenges, means potentially missing the game-changing winners that define entire markets. While the risks are real, the outsized rewards from successful B2C ventures prove that these challenges are worth taking on.