The End of the Startup as the Atomic Unit. The Rise of a New Breed of VCs

For decades, venture capital has been built around one clean unit of investment: the startup. One company, one cap table, one product, one founding team, one thesis, one financing round. A founder picked an idea, incorporated a company, raised capital, built a team, and committed the next seven to ten years of their life to turning that one company into something important.

This model made sense because startups are brutally hard. Focus matters. Context switching kills momentum. A company needs obsession before it earns the right to exist. So when VCs meet a founder working on five things at once, the instinctive reaction is usually simple: this person is not serious.

Most of the time, that reaction is probably right. A distracted founder can destroy a company before it even gets started. Many startups do not die because the idea was terrible; they die because the founder never gave the idea enough intensity for long enough.

But AI may force us to revisit this assumption. Not abandon it completely, and certainly not fund every founder with ten half-built demos and a vague story about optionality. But we may need to question whether the startup will always remain the first and only atomic unit of company formation.

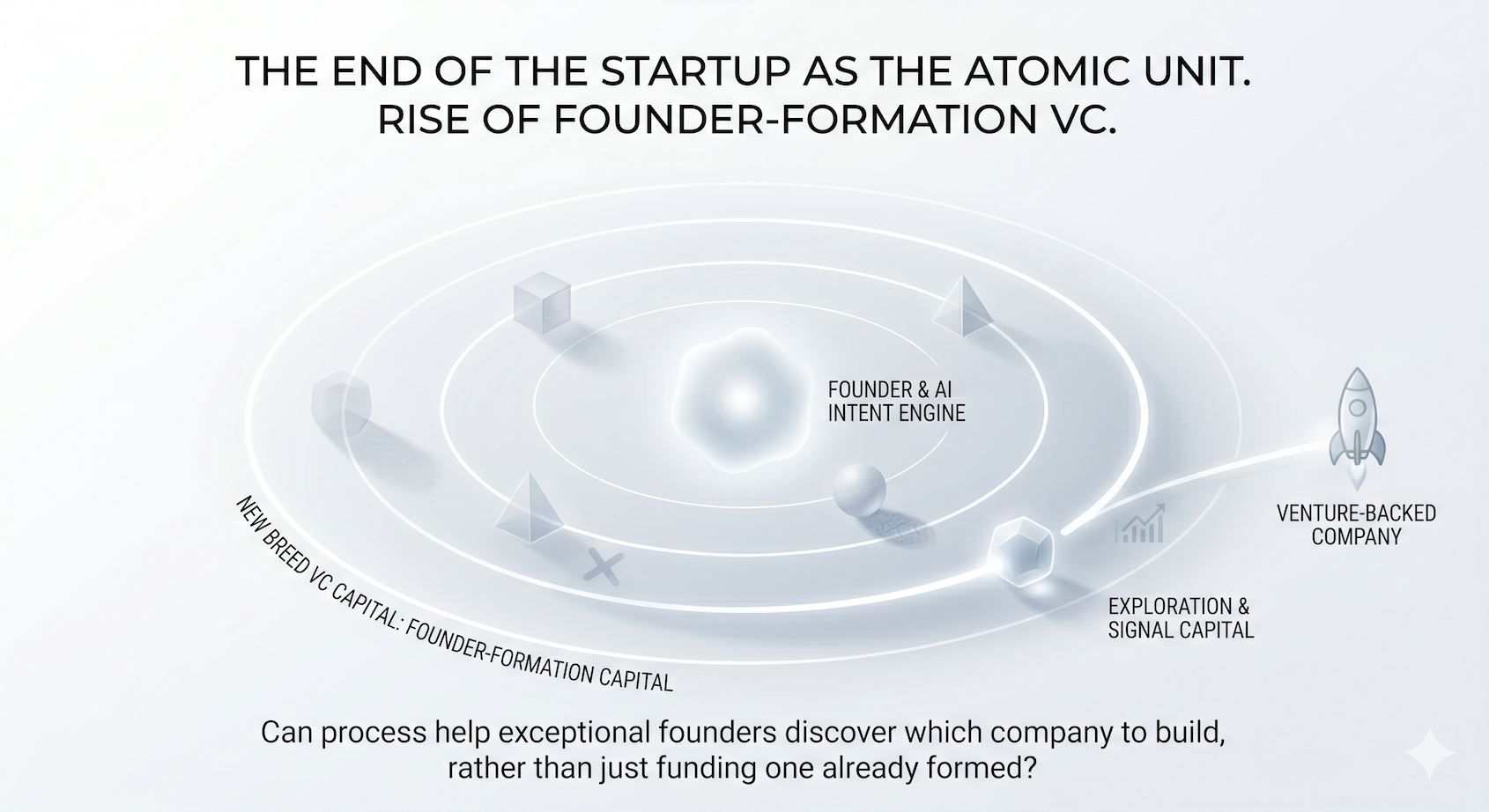

Because AI may create a new kind of founder: not someone building one startup from day one, but someone running a company-formation engine. This founder can test multiple ideas, launch small products, use AI agents and contractors, collect market signals, kill weak experiments quickly, and only later decide which experiment deserves to become a real venture-backed company.

Historically, this was possible only for rare outliers. Elon Musk could operate across Tesla, SpaceX, Neuralink, The Boring Company, X, and xAI. Jack Dorsey could move between Twitter and Block. Marc Lore could build company after company. These people were treated as exceptions: genius operators with unusual energy, unusual memory, unusual delegation ability, unusual access to talent, and unusual access to capital.

AI will not turn every founder into that archetype. That would be fantasy. But it may make some version of portfolio entrepreneurship more accessible. AI gives founders a kind of operating extension: memory, research, writing, coding, customer support, recruiting support, documentation, sales enablement, workflow coordination, and follow-up. It does not replace judgment, taste, courage, leadership, or obsession. But it does externalize a growing part of the founder’s operating load.

In the past, a founder had to hold too much in their own head: the product roadmap, customer feedback, investor updates, hiring pipeline, competitive research, financial model, user interviews, sales notes, technical decisions, internal meetings, strategic ideas, and all the follow-ups that should have happened but did not. Now, more of that can be captured, summarized, queried, automated, delegated to agents, connected to tools, and turned into workflows.

This may change the early company-formation process. The old path was idea to company to product to team to traction. The new path may become thesis to experiments to products to signals to commitment to company. The company may come later. The startup may become what a founder forms after the market starts pulling, not before.

And maybe this is not just a different way to build startups. Maybe it is also a way to reduce the risk profile of the companies that eventually get funded.

Today, many startups are formed around ideas that have not been tested deeply enough. A founder incorporates, raises capital, builds a small team, creates a cap table, and only then discovers that the market does not really care. The failure looks like a startup failure, but in many cases, it may have been a premature company-formation failure.

AI may allow founders to test demand, distribution, product behavior, customer pain, workflows, pricing, and early retention before wrapping the whole thing inside a venture-backed company. Weak ideas can die earlier. Stronger signals can earn more attention. The company that finally gets formed may begin with more evidence, more clarity, and less blind faith.

That does not eliminate startup failure. Nothing does. But it may reduce one category of failure: startups that should never have become startups in the first place.

That is the uncomfortable part for venture capital. Our model likes clean lines. We like one company, one cap table, one CEO, one founding team, one mission, one investor update, one board, and one financing path. We underwrite dedication, and for good reason. But what happens when the best early-stage founder has not yet chosen the company? What happens when the real asset is not one incorporated startup, but the founder’s ability to generate, test, learn, and compound multiple startup experiments?

This could create a new breed of VC firm. Not a classic venture studio, because the founder is not an employee. Not an accelerator, because the goal is not a batch program. Not a traditional pre-seed fund, because the investment is not necessarily into one fixed idea from day one. It may look more like founder-formation capital: a GP backs the person, their thesis space, their operating system, and maybe a few early experiments, with the understanding that one or two of those experiments may eventually become the real company.

This attacks one of VC’s sacred assumptions: we invest in focused founders building one company. The counter-question is more nuanced: what if, at the earliest stage, focus is not picking one idea too early, but building the discipline to test many ideas and know which one deserves obsession?

That distinction matters. This is not an argument for distraction. It is an argument for a more precise view of commitment. Some ideas deserve a weekend. Some deserve a prototype. Some deserve customer discovery. Some deserve a small team. Some deserve a company. Some deserve a venture-backed company. Not every idea deserves a startup, and AI may make that more obvious, not less.

For GPs, this does not make the job easier. It makes it harder. There will be more experiments, more prototypes, more micro-products, more AI-generated traction, more fake signals, more solo founders with ten demos, and more “companies” that are really just features. The noise will increase. But the signal may also change.

We may need to underwrite not only whether the founder is focused, but whether they know when to focus. Not only whether they can build fast, but whether they can kill fast. Not only whether they can launch multiple experiments, but whether they can recognize the one that deserves obsession. Not only whether a company has early traction, but whether it deserved to become a company in the first place. The real risk may not be that a founder starts with many experiments. The real risk may be that they never graduate from experimentation to commitment.

That graduation moment may become one of the most important moments for GPs to underwrite. Can this founder move from portfolio operator to company builder? Can they turn an experiment into an institution? Can they recruit a dedicated team around one wedge? Can they stop exploring when the market gives them a clear signal? Can they commit the necessary intensity once the opportunity deserves it?

If the answer is yes, then maybe the founder’s early experimentation was not a red flag. Maybe it was the search process. But if the founder cannot make that transition, then the whole thing remains a collection of clever demos, not a company.

This raises difficult structural questions for venture capital. Should some GPs create smaller experimental checks before a company is fully formed? Should we build founder-first vehicles that back a person and a thesis space rather than one incorporated idea? Should there be rights that convert into the winning company? Should we separate exploration capital from company-building capital? Can a GP provide studio-like support without turning the founder into an employee? How do we handle governance, ownership, conflicts, and commitment when the investable asset begins as a formation engine rather than a single startup?

I do not think the answers are obvious yet. In fact, the first versions of this model will probably be messy. Some will look like venture studios with better branding. Some will fund distracted founders who never commit. Some will create ugly cap table problems. Some will confuse experimentation with strategy. But that does not mean the question is wrong. It may simply mean the structure has not been invented properly yet.

The deeper point is that AI may not only change how startups are built. It may change when a startup should exist. It may separate the act of company formation from the act of experimentation. It may allow founders to test demand, distribution, product, and workflow before they wrap the whole thing in a venture-backed company.

For decades, the startup was the atomic unit of venture capital. Maybe in the next era, that assumption starts to break. Maybe the founder, not the startup, becomes the new unit of company formation. And if that happens, a new breed of VC firms may emerge: firms that do not just fund companies after they are formed, but help exceptional founders discover which company deserves to be formed in the first place.